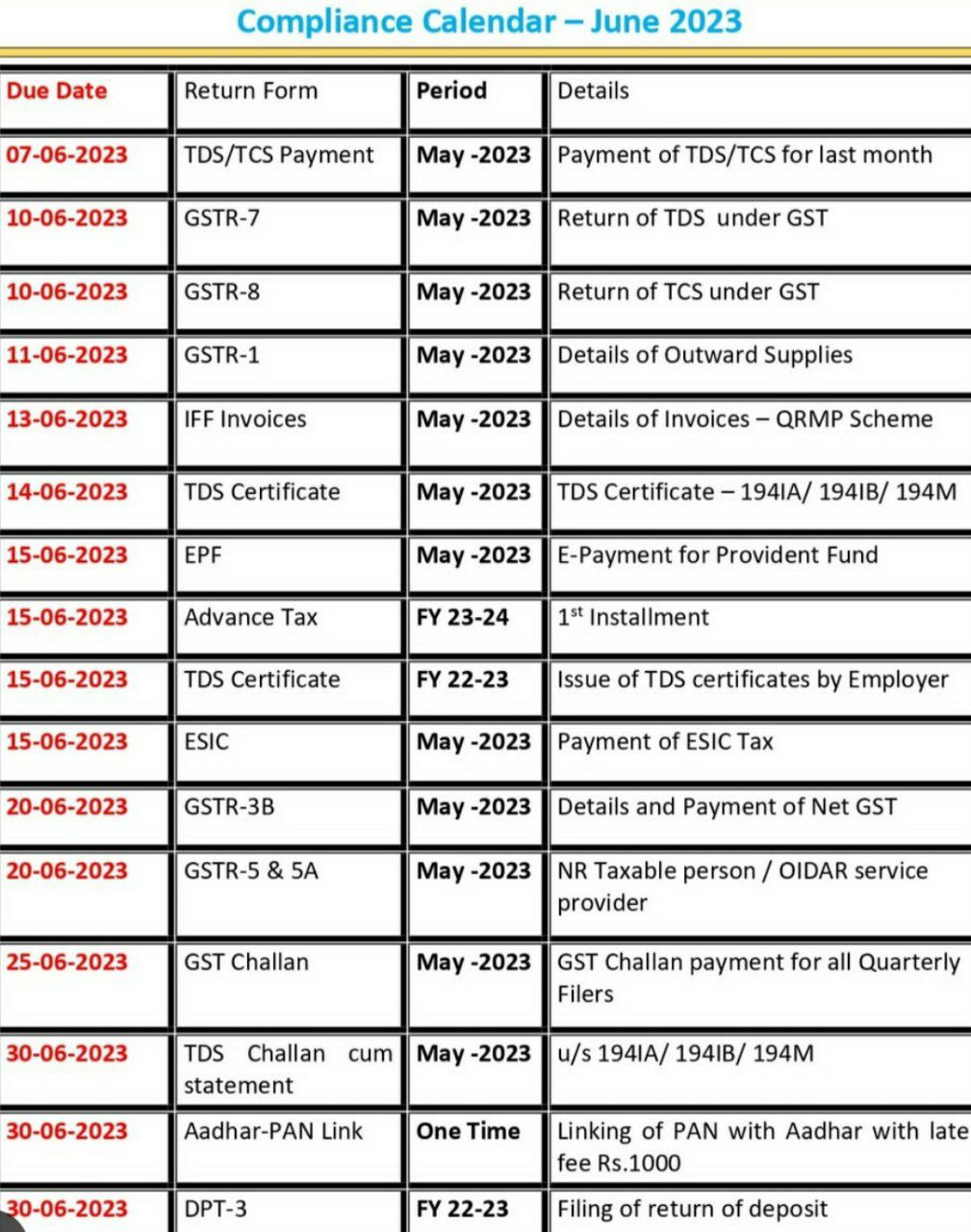

Compliance Calendar for the Month of June 2023

Compliance Calendar for the Month of June 2023

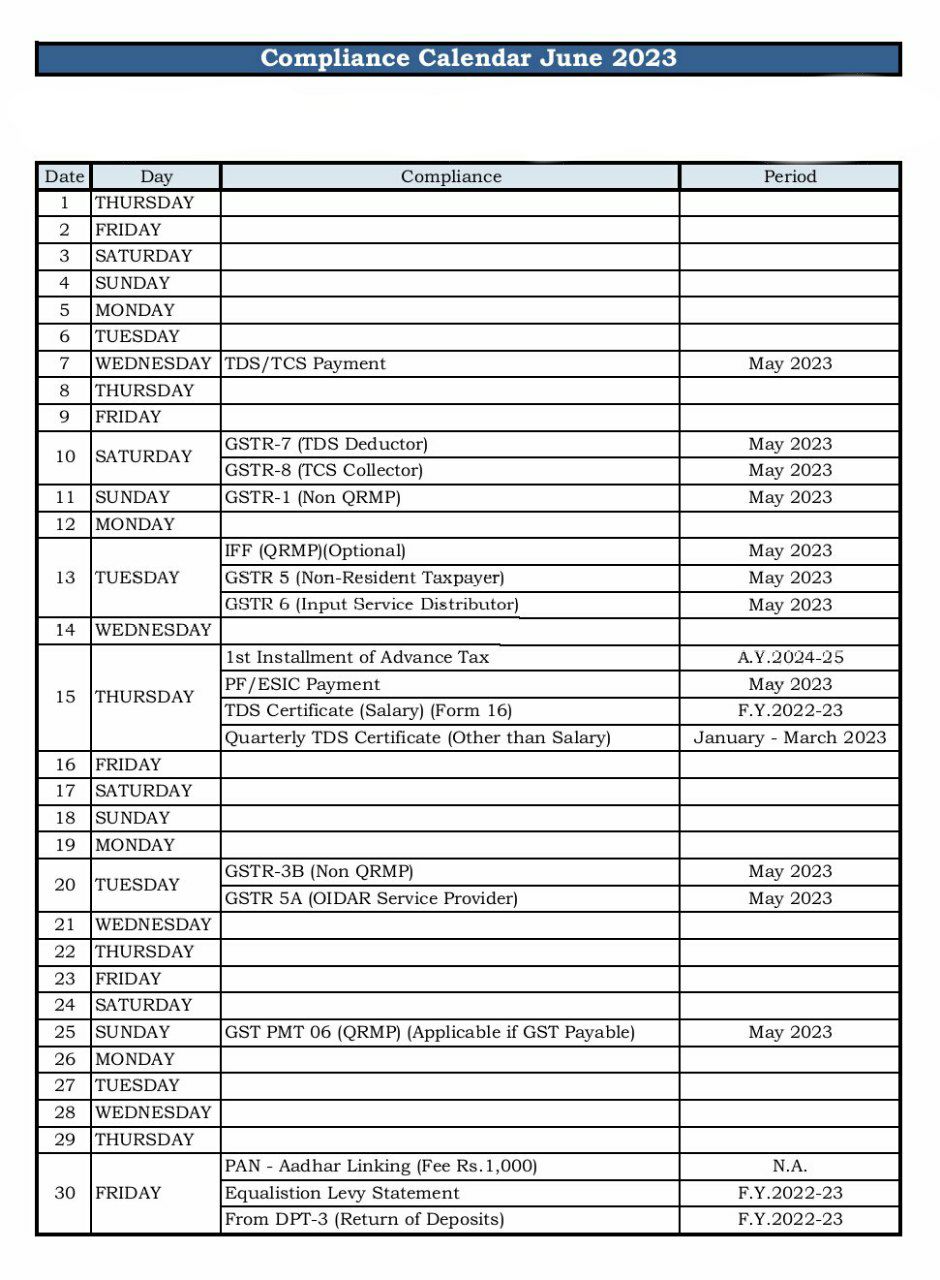

Statutory and Tax Compliance Calendar for June 2023

|

Statutory and Tax Compliance Calendar for June 2023

|

Gst Login Page:

http://www.gst.gov.in is the official Goods and Services tax website, widely known as the GSTN portal/ GST Portal, which facilitates many kinds of services for GST taxpayers, that is start from taking GST Registration, traversing via GST Return filing, GST Refund application filling, and GST registration cancellation application etc.

MCA allows you to look at the your company master data by just entering the company’s CIN. The master data of any LLP or company can be found at the website below.

http://www.mca.gov.in/mcafoportal/viewCompanyMasterData.do

PF Portal makes available a lot of its services online. It is useful to both Employer & Employee. Employee Provident Fund office also assists the Central Board in administering a mandatory contributory PF Scheme, an Insurance Scheme and a Pension Scheme for the workforce engaged in the organized sector in India.

https://unifiedportal-emp.epfindia.gov.in/epfo/

Employee State Insurance is a health insurance scheme and self-financing social security for Indian Employee managed by ESIC under the Employee State Insurance Act 1948. Under this scheme, employees earning up to Rs. 21,000 per month should contribute 1.75% towards Employee State Insurance while the employer contributes 4.75% which shall be deposited with the Govt within 15 days from the end of the respective month.

Employee State Insurance corporation is providing a wide range of services using online mode via its portal. Below is the link to Employee State Insurance Portal.

http://www.esic.in/employeeportal/login.aspx

This is the official website of CPC(Tax deduction at source), Department of Revenue, Ministry of Finance, Government of India.

Centralized Processing Cell (Tax deduction at source ) is a technology-driven transformation initiative for TDS administration that provides a comprehensive solution through its portal TRACES. The Portal has been developed under the National E-Governance Plan of the Govt.

Below online enabled services are available on this portal:

https://www.tdscpc.gov.in/app/login.xhtml

Challan Status Enquiry for Tax Payers:

Using this feature, taxpayers can track the status of their challans deposited in banks online.

This offers two type of TDS searches:

On entering Challan Identification Number (CIN) i.e. details such as BSR Code of Collecting Branch, Challan Tender Date & Challan Serial No.) and amount (optional)

The taxpayer can view the following details:

BSR Code, Date of Deposit, Challan Serial Number, Major Head Code with description, TAN/PAN, Name of Tax Payer, Received by TIN on (i.e. date of receipt by TIN)

– Confirmation that the amount entered is correct (if the amount is entered)

By providing TAN & TDS Challan Tender Date range for a specified financial year, the Income tax taxpayer can view the below details:

CIN No, Major Head Code with description, Nature of Payment, Minor Head Code

In case income tax taxpayer enters the amount against a CIN, the system will confirm whether it matches with the details of the amount uploaded by the bank or not.

https://tin.tin.nsdl.com/oltas/servlet/TanSearch

Challan Status Enquiry for Tax Payers : Taxpayers can track the status of their challans deposited in banks online with the help of this provided feature.

There have two type of searches available –

1st CIN based view, &

CIN based view:-

On entering Challan Identification Number (CIN i.e. details such as BSR Code of Collecting Branch, Challan Tender Date & Challan Serial No.) and amount (optional)

The taxpayer can view the following details:

BSR Code, Date of Deposit, Challan Serial Number, Major Head Code with description, TAN/PAN, Name of Tax Payer, Received by TIN on (i.e. date of receipt by TIN)

– Confirmation that the amount entered is correct (if the amount is entered)

2nd TAN based view.

Tax Deduction Account Number (TAN) can be applied through both offline and online mode. If a person want to apply for TAN through online mode he/she have to application in FORM NO. 49B.

Link of FORM NO. 49B:-

https://tin.tin.nsdl.com/tan/form49B.html

Nowadays, PAN (PERMANENT ACCOUNT NUMBER) can be applied online from anywhere. Applying for PAN is a simple and easy process in which the require data must be filled online & after filling correct detail once the form is submitted, some mandatorily document which require should be sent at the NSDL Center as specified. Later, in case of any changes or correction that can also be made online through service portal.

With the help of below link online application can be made for PAN on NSDL website :-

https://www.onlineservices.nsdl.com/paam/endUserRegisterContact.html

The refund originated on processing of ITR (Income-Tax Returns) by the CPC- Bangalore or Assessing officers are transmitted to the , CMP Branch, SBI or Mumbai (refund Banker) on the very next day of the processing for additional distribution to the taxpayers.

Refund could be sent in two defined mode:-

NECS / RTGS: To permit credit of refund straight to the bank account , then Taxpayers bank account no. (which of at least ten digits),Bank branch’s MICR (Magnetic ink character recognition) CODE & correct mentioned address is mandatory.

Paper Cheque: Correct address & Bank Account No. is mandatory.

Amount of the tax can be seen by taxpayer after 10 days of their refund which has been sent by the Assessing Officer to their refund banker , just by entering correct ‘Assessment Year’ & ‘PAN’ (PERMANENT ACCOUNT NUMBER) detail.

https://tin.tin.nsdl.com/oltas/refundstatuslogin.html

Online Income tax E-filing Portal – This is the official portal of Ministry of Finance, Income Tax Dept, Govt of India. Above said E-filing Portal has been developed as a Mission Mode Project under National E-Governance Plan. Aim of this income tax portal is to give one window access to income tax-related services for national citizens and related stakeholders.

https://portal.incometaxindiaefiling.gov.in/e-Filing/UserLogin/LoginHome.html?lang=eng

Online tax payment Facility, where the income tax taxpayer can submit online challan & fil it challan through the Internet. The income tax taxpayer must have a bank account with the selected bank’s Debit card/ Net-banking.

https://onlineservices.tin.egov-nsdl.com/etaxnew/tdsnontds.jsp

The Commercial Taxes Department is a pioneer in the use of information technology to offer fair and equitable tax administration. The majority of the Department’s critical functions are now available online. Key Dealer services such as Commercial Taxes Registration, returns & registrations are also available online. Key Online Dealer services are as follows:

https://www.tgct.gov.in/tgportal/

Popular Articles :

Income Tax Related Compliance

| DATE | FOR THE PERIOD | PARTICULAR |

| 02-03-2023 | Jan 2023 | Timeline for furnishing of challan-cum-statement in respect of tax deducted under section 194-IA/ 194-IB/ 194M |

| 07-03-2023 | Feb 2023 | Payment of Tax deduction at source / Tax collected at source by Govt. offices |

| 15-03-2023 | Financial Year 2022-23 | Fourth instalment of advance tax for the assessment year 2023-24 or Advance tax last date for assessee under section 44AD / 44ADA |

| 17-03-2023 | Jan 2023 | Timeline for issuance of Tax deduction at source / Tax collected at source certificate for tax deducted u/s 194-IA/ 194-IB/194M |

| 30-03-2023 | Feb 2023 | Timeline for furnishing of challan-cum-statement in respect of tax deducted under section 194-IA/ 194-IB/ 194M |

| 31-03-2023 | Financial Year 2021-22 | Nation By Nation Report in Form No. 3CEAD |

| GST RETURN | FOR THE PERIOD | PARTICULAR | Due date of Filling |

| GSTR-7 | Feb 2023 | Goods and Services Tax monthly return for Tax deduction at source Deductor . | 10-03-2023 |

| GSTR-8 | Feb 2023 | Goods and Services Tax monthly return for Tax collected at source Collector. | 10-03-2023 |

| GSTR-1 | Feb 2023 | GST (Goods and Services Tax) Monthly return for registered persons having turnover of more than INR 5 Cr. | 11-03-2023 |

| GSTR-6 | Feb 2023 | GST (Goods and Services Tax) Return for Input Service Distributor | 13-03-2023 |

| Invoice Furnishing Facility | Feb 2023 | Invoice Furnishing Facility for Quarterly return filers | 13-03-2023 |

| GSTR-5 | Feb 2023 | GST (Goods and Services Tax) for Non-resident foreign taxpayers | 13-03-2023 |

| GSTR-5A | Feb 2023 | Goods and Services Tax Return for Online Information Database Access and Retrieval services provider | 20-03-2023 |

| GSTR-3B | Feb 2023 | Goods and Services Tax monthly return to Pay due tax till last day of month. | 20-03-2023 |

| PMT-06 | Feb 2023 | Required to Monthly Tax Payment under Quarterly Returns with Monthly Payment | 25-03-2023 |

| Letter of Undertaking | Financial Year 2023-24 | Due date to apply for export without payment of tax. | 31-03-2023 |

| CMP-02 | Financial Year 2023-24 | Due date to opt for composition scheme under Goods and Services Tax | 31-03-2023 |

| Dates | Act | Nature of Due date |

| 7th Dec 22 | Under Income Tax | Deposit of Tax Deducted at Source / Tax collected at Source for the month of Nov 2022. But all sum deducted by an office of Govt shall be paid to credit of the Central Govt on the same day where tax is paid without production of an Income-tax Challan. |

| 7th Dec 22 | Under Income Tax | Eqalisation levy payment Timeline for the month of Nov 22 in respect of equalisation levy on “Specified services” |

| 15th Dec 22 | Under Income Tax | Timeline for issue Tax Deducted at Source certification for Income tax deduction U/s 194I-A for the month of Oct 22. |

| 15th Dec 22 | Under Income Tax | Timeline for issue Tax Deducted at Source certification for Income tax deduction U/s 194I-B for the month of Oct 2022. |

| 15th Dec 22 | Under Income Tax | Due date for issue Tax Deducted at Source certification for Income tax deduction U/s 194M for the month of Oct 2022. |

| 15th Dec 22 | Under Income Tax | Timeline for issue Tax Deducted at Source certification for Income tax deduction U/s 194S for the month of Oct 2022. |

| 15th Dec 22 | Under Income Tax | Tax Deducted at Source Certificate for Tax Deducted at Source deduction other than salary for the quarter July 22 to Sept 2022. |

| 15th Dec 22 | Under Income Tax | Form 24G by Govt officer where Tax Deducted at Source / Tax collected at Source for Nov 22 has been deposited without production of challan. |

| 15th Dec 22 | Under Income Tax | 3rd Installment payment of Advance Tax for Assessment year 2023-24. |

| 15th Dec 22 | Under Income Tax | Form No 3BB by a stock exchange for the month of Nov 2022. The said form to be furnished by stock exchange in respect of transactions in which client code has been modified after registering in the system. |

| 30th Dec 22 | Under Income Tax | Deposits of Tax Deducted at Source U/s 194-IA for the month of Nov 2022. |

| 30th Dec 22 | Under Income Tax | Tax Deposits of Tax Deducted at Source U/s 194-IB for the month of Nov 2022. |

| 30th Dec 22 | Under Income Tax | Deposits of Tax Deducted at Source U/s 194M for the month of Nov 2022. |

| 30th Dec 22 | Under Income Tax | Tax Deposits of Tax Deducted at Source U/s 194S for the month of Nov 2022. |

| 30th Dec 22 | Under Income Tax | Income tax Form no 3CEAD for a reporting year by a constituent entity resident in India, in respect of the international group of which it is a constituent if the parent entity is not obliged to file report U/s 286(2) or the parent entity is resident of a country with which India does not have an agreement for exchange of report etc. |

| 31st Dec 22 | Under Income Tax | Filing of belated or revised ITR for Assessment year 2022-23 for all Assessee (provided assessment has not been completed before 31st Dec) |

| Dates | Act | Nature of Timelines |

| 10th Dec 22 | Goods and Services Tax | GSTR–7 (Tax Deducted at Source Deducted) for the month of Nov 2022. |

| 10th Dec 22 | Goods and Services Tax | GSTR – 8 (TCS Collected by E-Commerce Operator) for the month of Nov 2022. |

| 11th Dec 22 | Goods and Services Tax | GSTR – 1 for the month of Nov 22 for taxpayer who does not opt Quarterly Returns with Monthly Payment Scheme under Goods and Services Tax. |

| 13th Dec 22 | Goods and Services Tax | Invoice furnishing facility for taxpayer who opt Quarterly Returns with Monthly Payment Scheme under Goods and Services Tax. |

| 13th Dec 22 | Goods and Services Tax | GSTR-6 (Return by Input Service distributor for the month of Nov 2022. |

| 13th Dec 22 | Goods and Services Tax | GSTR– 5 by non-resident taxpayers for the month of Nov 2022. |

| 13th Dec 22 | Goods and Services Tax | GSTR-5A by Online Information Database Access and Retrieval services service providers for the month of Nov 22. |

| 20th Dec 22 | Goods and Services Tax | GSTR 3B for the month of Nov 22 for the taxpayer having turnover more than INR 5 Cr in previous year. |

| 25th Dec 22 | Goods and Services Tax | Goods and Services Tax Nov 22 monthly payment for taxpayers who opt for Quarterly Returns with Monthly Payment Scheme under Goods and Services Tax Act . |

| 31st Dec 22 | Goods and Services Tax | Due date for GSTR 9 for Financial Year 2021-22. |

| 31st Dec 22 | Goods and Services Tax | Timeline for GSTR 9C for Financial Year 2021-22. |

| Dates | Act | Nature of Timelines |

| 15th Dec 22 | Provident Fund and Employee State Insurance | Provident Fund and Employee State Insurance payment for the month of Nov 2022. |

For taxpayers, the month of November 2022 is important since it has timelines for a lot of compliances with the Goods and Services Act, Income Tax Act, Companies Act, and LLP Act. You avoid costly fines, make sure to submit the aforementioned forms within the deadlines. As a result, we encourage you to plan ahead of time and finish all necessary filings before the time allotted and due date expire.

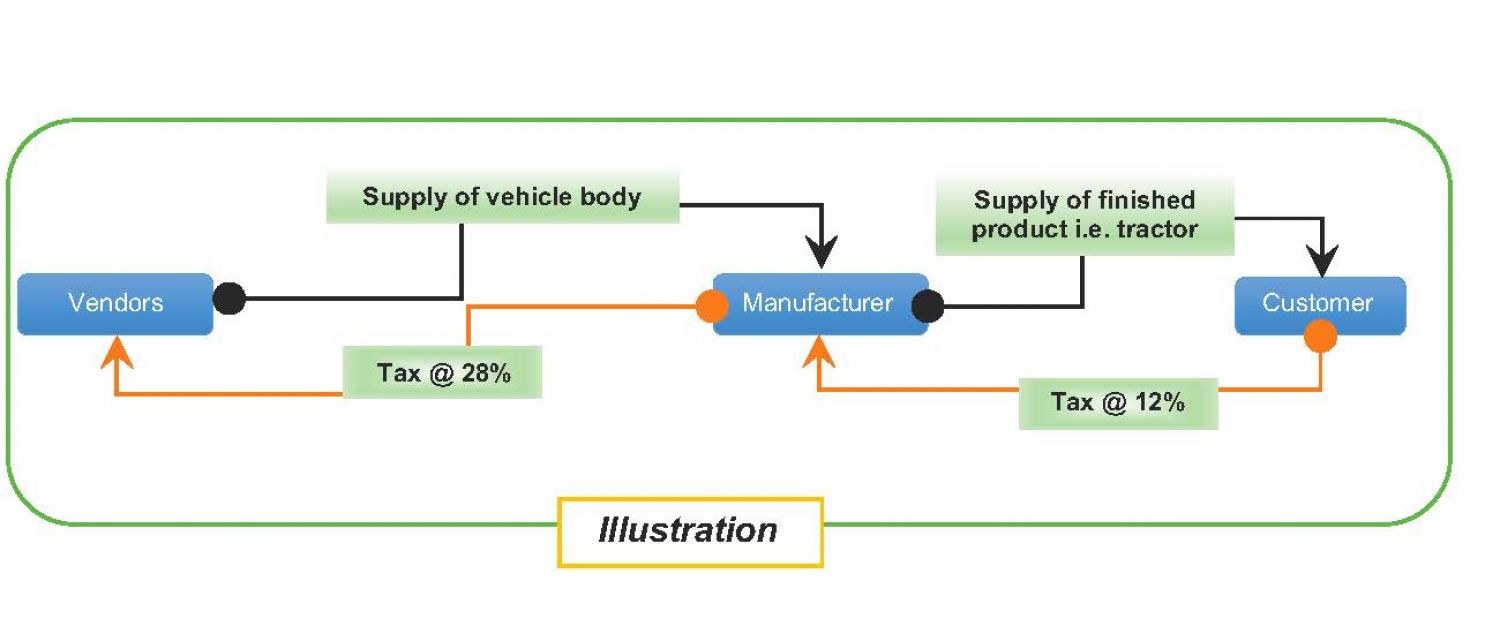

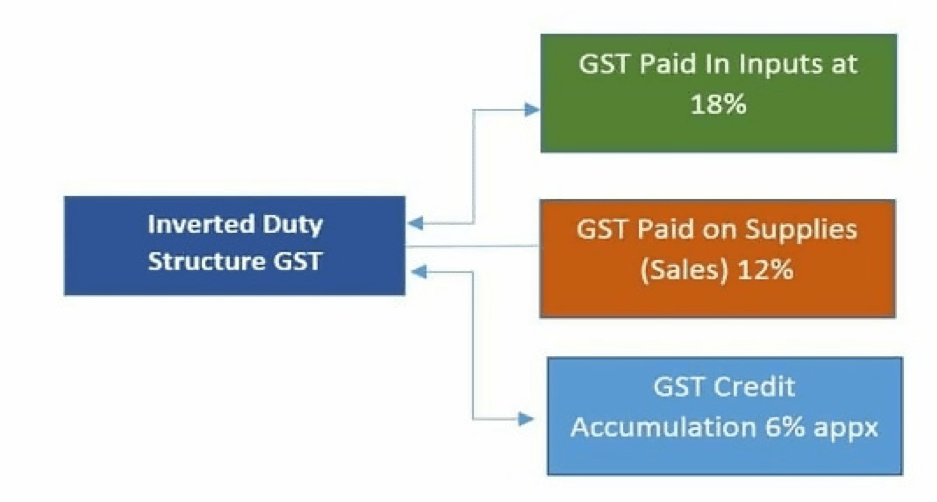

Below are some of the Circumstances in which tax paid on ITC is higher than the GST tax paid on outward supplies made.

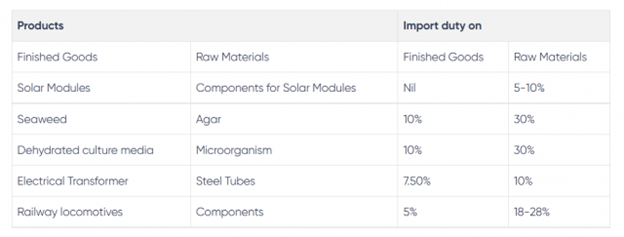

As seen above, raw materials are imported from other nations and used in the production or manufacturing of finished goods. Inverted duty structures place a higher tax on raw materials than on finished items.

Application filed for GST refund has to be attached by documentary or other evidence in order to establish that the amount of tax and interest, if any, paid on such tax or any other amount paid in relation to which refund is claimed was collected from, or paid by, him and incidence of such tax and interest had not been passed on to any other person.

The amount of GST tax & interest, if any, paid on that tax or any other amount paid in relation to which a refund is claimed must be supported by documentary or other evidence in order to show that the money was taken from or paid by the applicant and that the incidence of that tax and interest had not been passed on to another person.

List of documents required for inverse Duty Structure

GST Refund in case of Inverted Duty Structure, a GST taxpayer required to follow the Following Steps:

After the submission of a request for a GST refund, the GST taxpayer may follow up with the GST authority. In order to get the refund, the officer must give any documents or explanations that are required by the officer.

You can always get in contact with the GST Refund consultant at IFCCL if you are having difficulty obtaining your GST refund. Our “No Success, No Fee” policy is applied to GST Refund claims.