Is you don’t willing to Pay Income Tax ?

Is you don’t willing to Pay Income Tax ?

- The Financial Year 2022–2023 hopefully went well. The Next financial year about to start. However, let us know if it was successful in terms of your income tax planning. NO? The majority of us put off planning our income taxes until the very last day of the financial year, which results in us paying taxes on savings or hard-earned money, we could have made. If you are employee, have you given your employer the proofs of your tax saving investments made by us? You should be aware that In case you fail to give investment proofs, your company/employer will deduct more Tax Deducted at Source from your salary income.

Though the due date for certain filling changes, many firms needs that you file respective proof by the Month of March end.

- It is saddening to have to keep paying high taxes, even after investing under 80C and making other savings. But you can take the income tax refund from Income Tax Dept if you submit your tax returns within the time specified. Isn’t that great? Let’s examine the deductions and exemptions although you could still utilize even when the due date for filling your taxes documentation to your employer have cleared.

- Don’t worry; Non-salaried individuals are also eligible for the exemptions and deduction. The list of tax laws that could permissibly reduce your taxes for the current financial year is as follows:

1: Eligible deductions under Section 80C, in which you can claim deductions upto Rs.150000-

You may claim deductions upto 1,50,000 INR where you can eligible Deductions under Section 80C.

SCSS (Senior Citizens Savings Scheme)

- Senior Citizens Savings Scheme is only for elderly adults, those who have chosen to retire at the age of 55 or those who at least 60 years old.

- A National Savings Certificate must be purchased with a minimum deposit of INR 100. The investment tenure of an National Savings Certificate is 5 Years. You could demand that upon maturity, the entire amount be refunded to their account. If the National Savings Certificate funds are not claimed, they are all added to the plan. You can receive interest at 7.4%.

Fixed Deposit- Tax Saving

- Early withdrawal is not allowed when Bank fixed deposits have a five-year lock-in period despite of that they are still eligible for Section 80C deductions. The Interest on a five-Year Fixed Deposit is taxable but not eligible for tax breaks. Section 80C permits a tax deduction on investments of up to One and Half Lakhs. It could be opened by Indian citizens who can avail an advantage from interest rates ranging from 5.5% to 7.75%, it depends on the bank. All interest income from Fixed Deposit investments is taxable, and the minimum investment amount for Fixed Deposit’s is INR 1,000/-.

PPF (Public Provident Fund)

- Tax deductions for annual Public Provident Fund contributions are allowed U/s 80C of Income tax law. Public Provident Fund is a govt sponsored scheme, that offers you sufficient returns. A minimum of Rs. INR 500/- & a maximum of INR 1,50,000/- can be invested annually under this Scheme. Public Provident Fund has a fifteen-year lock-in period.

Sukanya Samridhi Yojana

- This tax-saving plan has only one saving strategy: to support young girls’ development. Sukanya Samridhi Yojana Saving Scheme is being offered for a young girl who is eligible for tax advantages. The Girl’s Parent or legal guardians are allowed to open an Bank account under Sukanya Samridhi Yojana Saving Scheme until Ten Years of her age. Whenever there are twins, Sukanya Samridhi Yojana Saving Scheme is extended with a third child and it is open to 2 girls’ child. It takes 15 years to deposit the money, and it matures period is 21 years. The interest rate of this scheme is 7.60% per year. There is a minimum investment needed of INR 250 and a maximum investment limit of INR 15 lakhs.

Life Insurance

- One way to ensure your family’s financial future after your passing is to protect them with a term insurance plan. However, did you know before that the premiums for these life insurance policies also allow you to reduce your tax liability?

- The answer is that section 80C allows for a tax deduction for life insurance premiums.

-

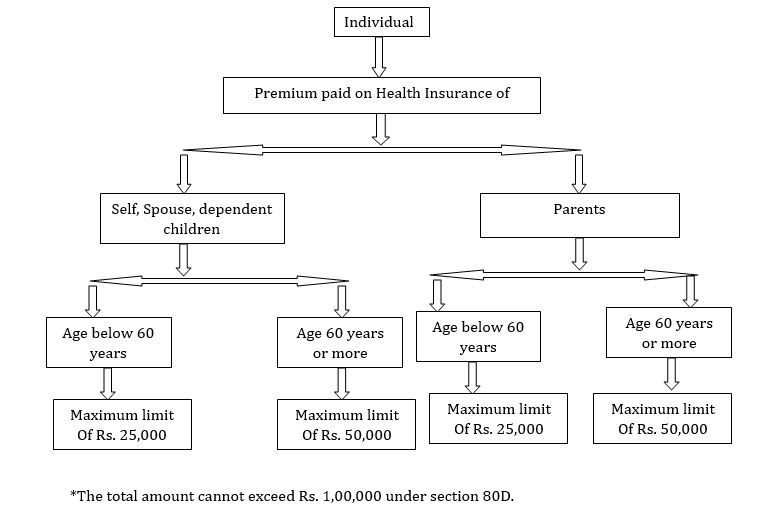

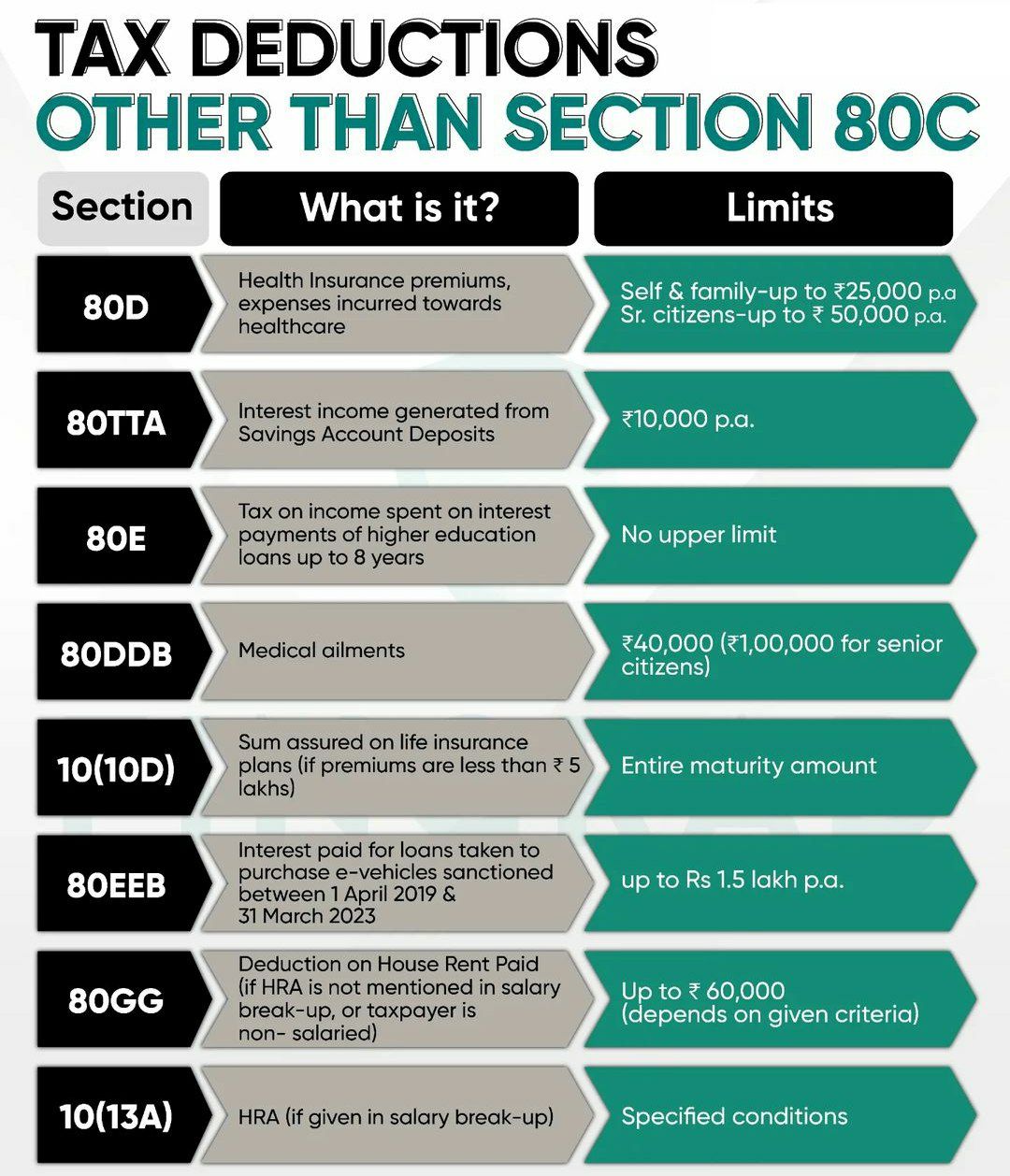

Benefit of U/s Medical Insurance Premium: Section 80D

- As per the Section 80D of income tax law, it permits claiming deductions form the gross Taxable Income for the payment of Insurance Premiums. If you pay for medical expenses for yourself, children or spouse you are allowed to deduct up to INR 25,000 yearly basis. The maximum income tax deduction for senior citizens medical insurance premiums is INR 50,000. Moreover, you may take the deductibles up to INR 25,000, if you spend the money on your parents’ behalf.

-

Benefit of U/s Charitable Donations Made: Under Section 80G

- You must keep the payment receipt from the financial year in order to claim a deduction u/s 80G. Eligibility of 50% to 100% of the total sum donated to the charitable trust may be deducted from your taxes as deduction of Charitable Donations u/s 80G. you should make sure to verify whether trusts or charitable institute are registered u/s 12A of income tax act, that they have qualified by section 80G certificate. Donations made in cash that are more than 2,000 INR cannot be considered as deducted, so donations over and above INR 2,000 should be made in another way. U/s 80C, contributions made to the Provident fund A/c are eligible for a Income tax deduction of up to Rs 1,50,000.

-

Rent paid to House: U/s 80GG

- Those people who are living in a rental house are eligible for deductions U/s 80GG. But, this tax deduction is only allowed or available to those who are not salaried class people and do not receive a HRA allowance from their employers.

-

Benefit of U/s 80D : Health Insurance

- These days, everyone must purchase health insurance due to the rising cost of medical care bill or cost. If you pay the insurance premiums for your health insurance, you can save up to INR 15k to 20k U/s 80D because it aids in helping you pay for your medical bills in an emergency situation.

-

Benefit of U/s 80E : Education Loans

- According to Section 80E, the interest paid on student loans for higher education is still exempt from taxes for the borrower, their kids & their spouse, An person may deduct the amount of Interest paid by him, not the principal amount paid by him.

-

Benefit of U/s 80EE : Home Loans

- One of the best ways to reduce income tax in India is to take out home loans. Presently current situation, house Loans have helped in decrease taxable income. First-time homebuyers may use Section 80EE to deduct up to INR 50,000 from the interest paid on a house Loans over the throughout a Financial year.

-

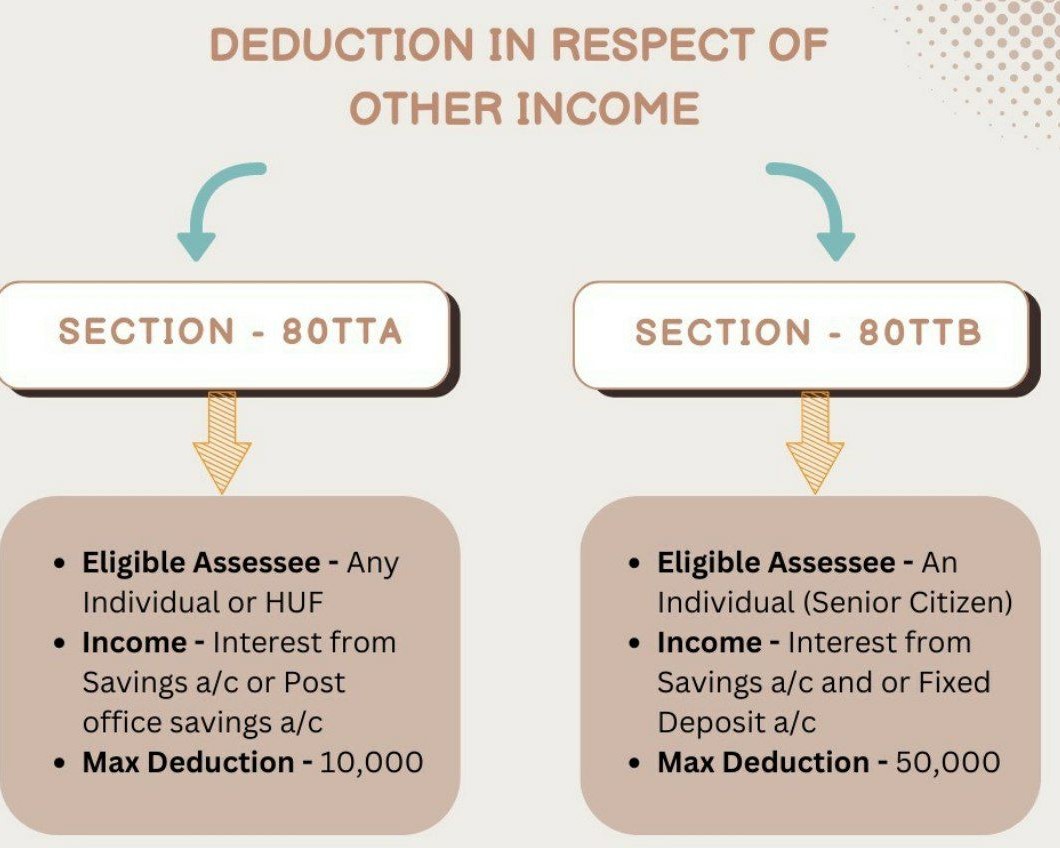

Interest on saving Accounts: Section 80TTA:

- Interest earned on savings accounts is deductible u/s 80TTA. Although any interest income acquired on a savings bank account over INR 10,000/- would be recognized as a taxable income.

Conclusion.

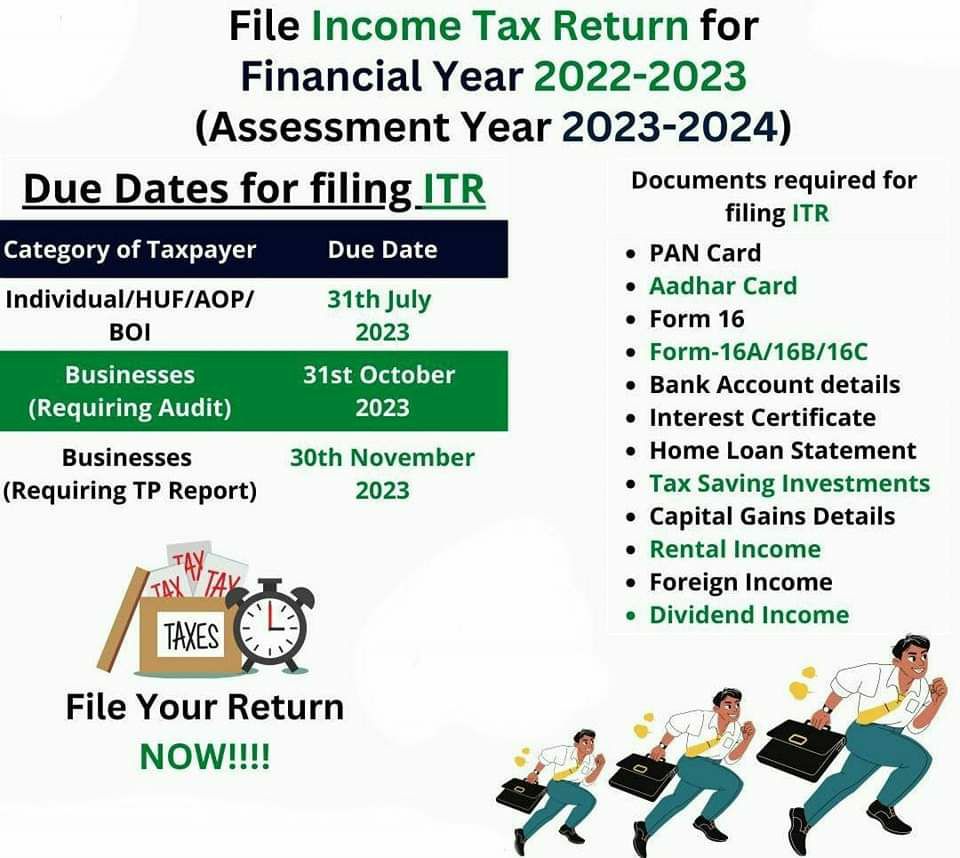

For your convenience, those who have already made above invested should please file their investment proofs on or before dead line or on time, and those who haven’t should invest before the end of March. You can still can file & make your claim in your ITR for Financial year 2022–23 and receive the income tax refund if you are an employee and missed the Due Date to provide your employer with the necessary documentation.

Post Written By : Associates – Tarun Kumar