DOCUMENTATION OF AUDIT & WORKING PAPER FOR AUDIT

DOCUMENTATION OF AUDIT & WORKING PAPER FOR AUDIT

The skill of an accountant can always be ascertained by an inspection of his working papers.

Documentation Standard on Auditing (SA) 200, “Basic Principles Governing an Audit” (Paragraph 11), states, “The auditor should document matters which are important in providing evidence that the audit was carried out in accordance with the basic principles.”

Documentation, for purposes of this Standard, refers to the working papers prepared or obtained by the auditor and retained by him, in connection with the performance of his audit.

Documentation of Audit & Working Papers for Audit: Audit documentation and working papers are essential to support the audit process, ensuring accuracy, compliance, and providing evidence for the auditor’s findings. They serve as a record of the work done, the conclusions reached, and the basis for the auditor’s opinion.

Working papers for Audit :

- aid in the planning and performance of the audit;

- aid in the supervision and review of the audit work; and

- provide evidence of the audit work performed to support the auditor’s opinion.

Components of Audit Documentation & Working Papers

- This comprehensive documentation and working paper framework helps ensure a thorough and compliant audit process.

- Planning Documentation: Outline the audit strategy and detailed audit plan. Identify and assess the risks of material misstatement. Agreement between auditor and client outlining the audit’s scope and objectives.

- Keep working papers well-organized and indexed. Ensure that documentation is clear, concise, and comprehensive. Regularly review working papers to ensure accuracy and completeness. Maintain confidentiality and security of all audit documentation. Follow regulatory requirements for the retention period of audit working papers.

- Indexing and Cross-Referencing : Each working paper should be properly indexed and cross-referenced to ensure easy retrieval and review.

- Content of Working Papers : Audit working paper cover page with client name, audit period, and description. State the objective of the working paper. Document the audit procedures performed. Include copies of documents, ledgers, vouchers, and other evidence. Note the findings and observations. & Summarize the conclusion based on the evidence and findings.

- Documentation of Findings : Document all findings, discrepancies, and issues identified during the audit. Obtain written representations from management regarding key aspects of the audit. Summarize conclusions drawn from the audit procedures performed.

Types of Working Papers

The working papers are classified as follows : Permanent Audit Files & Current Audit Files

- Permanent File: Contains information of continuing importance, such as the engagement letter, organizational chart, internal control documentation, and previous year’s audit reports.

- Current File: Contains documentation for the current year’s audit, such as financial statements, audit programs, trial balances, and supporting schedules.

A permanent audit file normally includes:

- Copy of initial appointment letter if the engagement is of recurring nature

- Record of communication with the retiring auditor, if any, before acceptance of the appointment as auditor

- NOC from previous auditor

- Information concerning the legal and organisational structure of the entity.

- In the case of a company, this includes the Memorandum and Articles of Association.

- Organizational structure of the client

- List of governing body including Name, Address and contact details. For

- Instance, the List of Directors in case of a company, List of partners in a

- partnership and list of Trustees in a Trust.

- Extracts or copies of important legal documents, agreements and minutes

- relevant to the audit.

- A record of the study and evaluation of the internal controls related to the

- accounting system. This might be in the form of narrative descriptions,

- questionnaires or flow charts, or some combination thereof.

- Copies of audited financial statements for previous years

- In the case of a statutory corporation, this includes the Act and Regulations under which the corporation functions

- Analysis of significant ratios and trends

- Copies of management letters issued by the auditor, if any.

- Notes regarding significant accounting policies.

- Significant audit observations of earlier years.

- Assessment of risks and risk management

- Major policies related to Purchases and Sales

- Details of sister concerns

- Details of Bankers, Registrars, Lawyers etc

- Systems and Data Security policies

- Business Continuity Plans

A Current audit file normally includes:

- Correspondence relating to acceptance of annual reappointment.

- Extracts of important matters in the minutes of Board Meetings and General

- Meetings, as are relevant to the audit.

- Evidence of the planning process of the audit and audit programme

- Analysis of transactions and balances.

- A record of the nature, timing and extent of auditing procedures performed, and the results of such procedures

- Evidence that the work performed by assistants was supervised and reviewed.

- Copies of communications with other auditors, experts and other third parties

- Copies of letters or notes concerning audit matters communicated to or

- discussed with the client, including the terms of the engagement and material weaknesses in relevant internal controls.

- Letters of representation or confirmation received from the client.

- Conclusions reached by the auditor concerning significant aspects of the audit, including the manner in which exceptions and unusual matters, if any,

- disclosed by the auditor’s procedures were resolved or treated.

- Copies of the financial information being reported on and the related audit reports.

- Audit review points and highlight.

- Major weakness in Internal control

Examples of Specific Working Papers for Tax audit

- Audit Plan and Risk Assessment

-

- Engagement Letter

- Preliminary Risk Assessment

- Audit Planning Memo

- Financial Statement Working Papers

-

- Balance Sheet Schedules

- Profit & Loss Account Schedules

- Cash Flow Statement Analysis

- Ledger and Journal Review

-

- General Ledger Review Sheets

- Journal Entry Testing Worksheets

- Bank Reconciliation Working Papers

- Tax Compliance

-

- TDS Compliance Checklist

- GST Compliance Checklist

- Advance Tax Payment Verification

- Supporting Documents

-

- Sample Invoices

- Sample Vouchers

- Bank Statements

- Critical Area Verification

-

- Fixed Assets Verification Schedule

- Inventory Count Sheets

- Related Party Transaction Documentation

- Audit Findings and Reports

-

- Summary of Audit Findings

- Management Representation Letter

- Form 3CA/3CB and 3CD

- Additional Documents (if applicable)

- New Clause 4 inserted

- Identity proof

- Residence/Address Proof

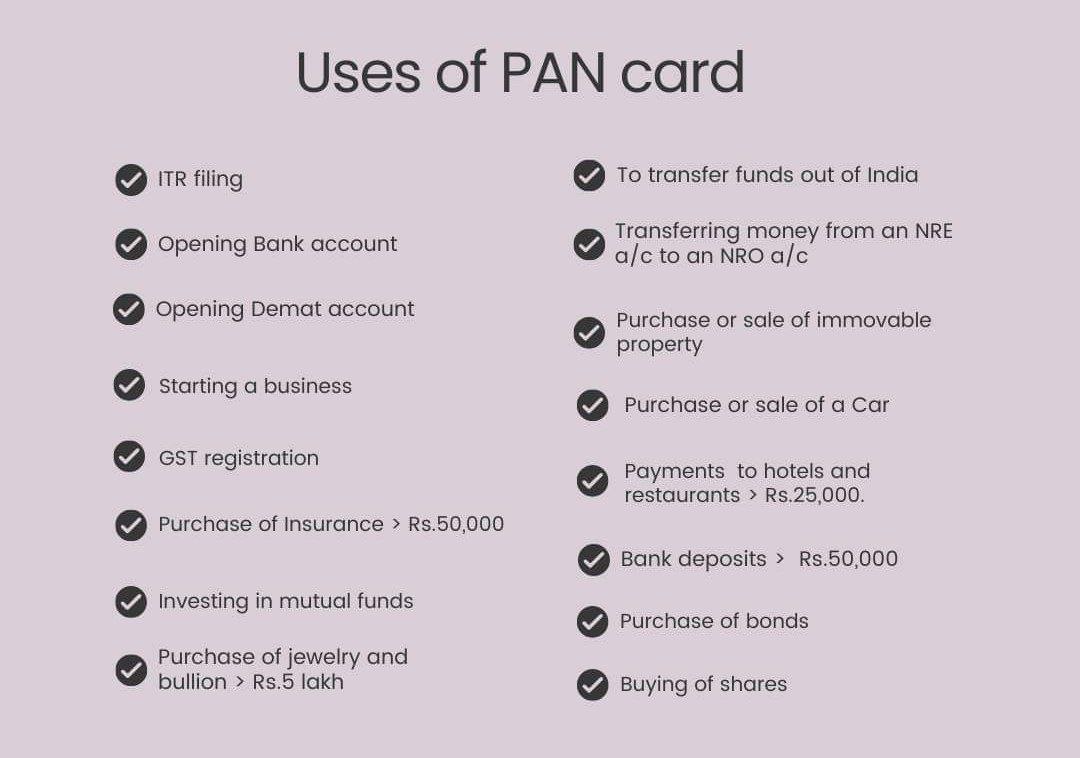

- PAN Card

- In case of

- An individual : a propritary letter/Shops and Establishment Licence

- A firm : Partnership deed ; Registration Certificate

- A company – Certificate of incorporation; Certificate to commence business (in case of public companies)

- Any other entity : Incorporation/registration certificate or formation deed

- Last Balance Sheet or date of commencement of business

- Partners and their Profit Sharing Ratios

- Partnership Deed Amendment or Addendum to Deed of partnership

- Nature of Businesses or Professions

- Management Representation letter

- Extracts of Objects Clause of the Memorandum of Association

- Extract of the Deed of Partnership

- Sales Tax/ VAT registration Certificate

- Excise Registration certificate

- Any other specific registrations such as NBFC,

- Chemists and Druggists etc.,

- Copy of last return of income filed

- List of Books maintained

- Rates of depreciation applicable to each type of asset

- Extracts of Fixed Assets Register

- Details of loans and advances to and from related parties

- Documentary evidence depending on nature of capital receipt and reasons for not crediting the profit and loss account

- Copies of bills in respect of assets purchased during the audit period

- Details of fixed assets sold, scrapped or discarded or impaired

- Computation of addition/reduction in value on account of MODVAT Credit or exchange difference or Government subsidy

- Details of contingent liabilities

- Amounts Admissible various clauses of – {Clause 19} [Old Clause 15]

- Details of such expenses and the category of such assets

- Documentary evidence as to its payment/receipt-

- Amount Paid / Received from the Employees

- List of employees and their salaries, applicability of PF and the contribution of the employer/employee

- Terms of employment, In case of any agreement with any trade union, copy thereof

- Amount Debited to Profit and Loss Account

- Query sheet in respect of Ledger Scrutiny

- Details of such payments on scrutiny of such expenses/cash or bank book, receipts thereof.

- Management representation letter

- Note on such expenses

- Certificate from the assessee

- Details of such payments made

- Relevant query sheet

- Amounts paid and the amounts payable as per law

- List of contingent liabilities

- Contingent liabilities provided for in the books of accounts

- Details of Total income

- Details of Exempt income

- Amount of Interest u/s. 23 of MSME Act, 2006

- Correspondence with suppliers ascertaining their registration under the MSMED Act, 2006

- Management representation letter

- Amounts outstanding to such enterprises

- Calculation of interest

- Payments made to Persons specified u/s. 40A(2)(b)

- Details of specified persons under Section 40A(b)

- Ledger Scrutiny and the scrutiny of cash and bank books

- Deemed to be Profits

- Types of business

- Profits during the period

- Transfer of profits to Reserve/Fund and investment thereof as per law

- Board resolution

- Sum Referred u/s.43B

- List of payments specified in Setion 43B

- The provisions made thereof

- The amounts paid thereof

- Brought forward loss or depreciation

- Last Assessment Order(s)

- Last Return(s) of income filed

- Chapter VI A –Documents :

- 80 C – Copy of Receipts Copies

- 80 D – Copy of Insurance Premium Receipts

- 80 E – Copy of Interest statement or Payment confirmation

- 80 G – Copy of deduction Certificate or the payment receipt

- 80 IA, IAB, IB, etc. – Copy of Chartered Accountant Certificate.

- Details of capital gains transactions

- Evidence of deductions claimed under various sections

- Any law requiring the assessee to maintain the books of accounts for such businesses e.g.

- professionals under the Income Tax Act, 1961;

- Final statement of accounts for the year under audit and the immediate preceding financial year.

- Details of related party transactions

- Whether Section 145A applicable

- Traders under the VAT Laws etc.,

- Last audit report

- Details of foreign transactions and foreign assets

- Provisions of law such as companies can maintain only accrual method of accounting

- Deviation, if any and the quantification thereof.

- Details of the Capital Asset, Reasons for conversion, Impact of conversion

- Claims made and Refund Orders

- New Clause 4 inserted